Top Processors. Exclusive Rates. That's Maverick Match.

Answer a few questions about your business and get personalized payment processor recommendations paired with discounted partner rates you won't find anywhere else.

Get Matched💳 Save money on credit card processing with one of our top 5 picks for 2026

Understanding basis points allows you to calculate how much your credit card processor is truly charging you. Learn what basis points are and how they affect your business's payment processing costs.

WRITTEN & RESEARCHED BY

Expert Contributor

Last updated onUpdated

REVIEWED BY

Editor & Senior Staff Writer

Negotiating credit card processing rates can be a daunting prospect for a merchant.

You need to understand what a fair cost for processing is, especially in your particular industry and based on your business model. You also need to be able to take the rates you’re quoted and put them into real-world numbers.

You’re probably familiar with percentages and percentage points already — but you might also hear the phrase basis points (BPS) in your negotiations. If you’re not a finance whiz, this might throw you off a bit.

The good news is, basis points are really easy to understand. I’m here to explain them to you and show you how they affect your processing costs.

Warning: Math ahead! (Disclaimer: It’s not scary math.)

Table of Contents

A basis point is equal to one-hundredth of a percentage point: 0.01% (or 0.0001 written in decimal form). It’s the smallest unit of measurement used to describe interest rates, processing rates, and yields on financial products (such as bonds).

One hundred basis points equal 1%.

Yes, it’s that simple.

One of the arguments in favor of basis points is that it’s a way of removing ambiguity from statements involving numbers, and changes in numbers. Say for example, the standard yield rate is 8.5% and it increases 3.5%. Is that now 12%, or 8.85%?

Basis points eliminate room for misinterpretation of numerical statements: if the yield rate is 8.5% and increases 350 basis points, that’s an increase to 12% — if it’s 35 basis points, that would be 8.85%.

Where credit card processing is concerned, you’re more likely to encounter basis points in discussions of card processing rates.

Here are a couple of contexts in which you might see basis points referenced:

However, there are a couple of things to keep in mind:

If you’re on an interchange-plus plan, the markup your processor quotes you isn’t the entirety of what you’ll pay — you still need to pay interchange fees, which are the rates set by the card networks — Visa, Mastercard, Discover, American Express.

(If you’re on a tiered pricing model, you might also be quoted a markup percentage.)

To account for their interchange costs, processors typically charge a flat fee in addition to the percentage markup, to the tune of $0.10 to $0.25 per transaction. This is important because a change in basis points can easily be offset by a change in this flat fee.

It’s time to play with some numbers and calculate how changes to your basis points could affect how much you pay!

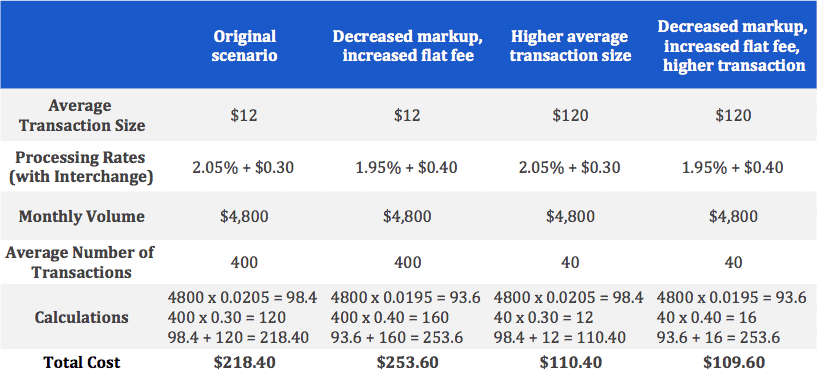

Let’s set an interchange rate of 1.8% + $0.10 (note: interchange rates vary by card network, type of card, and type of transaction. This is just one example). Your processor offers you a 0.25% markup (that’s 25 basis points) plus a flat fee of $0.20 per transaction, bringing your total processing cost to 2.05% + $0.30. Your average transaction size is $12.

If you know the interchange fee, you can calculate how your processor’s markup (in terms of basis points plus their flat fee) will affect how much you pay with the following equation:

12 x 0.0205 = 0.246

Rounded up, that’s $0.25 + $0.30, or $0.55 in processing costs for a $12 transaction, leaving you with $11.45.

But what if that changed? Say your processor lowered your markup to 15 basis points (0.15% over interchange) but raised your per-transaction costs 10 cents to $0.30. Your new rate, including interchange fees, would be 1.95% + $0.40. How would that change what you pay?

12 x 0.0195 = 0.234 or ~$0.23

$0.23 + $0.40 = $0.63

$0.63 > $0.55

In this example, your basis point savings are offset by the increase in your flat fee. Beware of this issue—do the math instead of just assuming it will translate to bigger savings!

But that’s just one transaction. How does this play out on a larger scale? Let’s go back to our original example, but also look at what happens when you up the average transaction size, or decrease the markup percentage but increase the flat fee.

As you can see here, changing even just one variable in the equation can have a dramatic effect on your processing rates. And if your average ticket size is small, the flat per-transaction fee can be more costly than the interchange and percentage markup. That makes it very important to do the math on your processing costs.

Also, remember that interchange rates vary from one type of transaction to another. So, the true cost of each transaction will vary from one sale to the next, regardless of how your processor bills you.

Further complicating the matter, processors often charge monthly or annual fees in addition to their per-transaction markup, which, of course, adds to your total processing costs.

Educated merchants make for good merchants. That’s why we’re here — to share our expertise and give you the knowledge you need to succeed.

If you don’t understand basis points or the other aspects affecting your credit card processing rates, do some research or ask someone to explain it to you. If your processor can’t do that, you probably want to start looking for a new one. You can start by checking out our top-rated credit card processors for small businesses.

Even if you are a small merchant, you have power. You do not have to accept the first offer a merchant account provider gives you. Educate yourself about your options. Know the risks in your industry. And if you need help securing a good deal on processing, check out our guide to negotiating with card processors.

Want to help shape the future of the Merchant Maverick website? Join our testing and survey community!

By providing feedback on how we can improve, you can earn gift cards and get early access to new features.

Help us to improve by providing some feedback on your experience today.

The vendors that appear on this list were chosen by subject matter experts on the basis of product quality, wide usage and availability, and positive reputation.

Merchant Maverick’s ratings are editorial in nature, and are not aggregated from user reviews. Each staff reviewer at Merchant Maverick is a subject matter expert with experience researching, testing, and evaluating small business software and services. The rating of this company or service is based on the author’s expert opinion and analysis of the product, and assessed and seconded by another subject matter expert on staff before publication. Merchant Maverick’s ratings are not influenced by affiliate partnerships.

Our unbiased reviews and content are supported in part by affiliate partnerships, and we adhere to strict guidelines to preserve editorial integrity. The editorial content on this page is not provided by any of the companies mentioned and has not been reviewed, approved or otherwise endorsed by any of these entities. Opinions expressed here are author’s alone.